Do you remember the car manager Ignacio López? He was a red flag for suppliers and, in the end, caused the biggest image loss of all time for the car companies for which he had often extracted gigantic discounts at suppliers’ expense.

Opel needed years to recover from the poor quality of the components used. As chief buyer, López squeezed the prices of the supplier industry until they finally had to produce as “cheaply as possible.”

It was consumers who paid for this debacle. They got vehicles that were extremely poorly assembled or had serious quality defects. The image of the OEMs involved suffered to the greatest extent possible.

The crisis in chips, energy and raw materials

Since the chip and raw materials crisis, a phenomenon has developed among many premium manufacturers. Fewer vehicles are being sold because components are missing, but profits have increased dramatically. Less is sometimes more, as the famous saying goes.

By concentrating on expensive vehicles, manufacturers have managed to do brisk business on the backs of consumers and suppliers, despite the crisis. But this could come to an end in the near future.

Suppliers under pressure

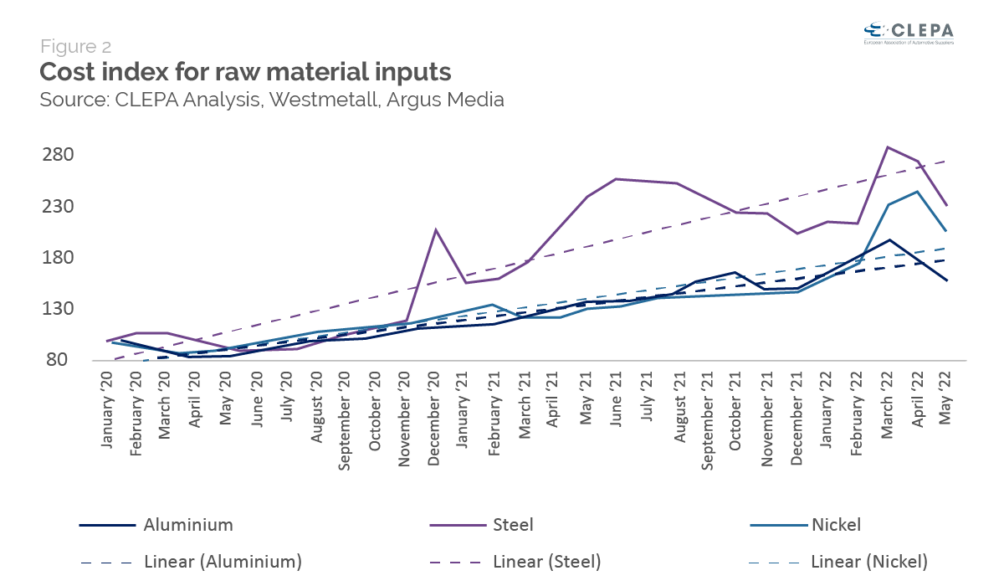

The European supplier industry association, CLEPA, is sounding the alarm. The European Association of Automotive Suppliers represents over 3,000 companies that supply the automotive industry.

For some time now, a nasty effect has been taking hold: Medium-sized suppliers in particular are having severe problems pushing through higher prices. As is so often the case in this industry, they are bound by long-term contracts. This means that due to the dramatic increases in energy and raw material prices, including as a result of the Ukraine war, some parts must even be supplied to OEMs below cost. In fact, 69 percent of suppliers said they were having problems passing on increased costs to OEMs.

Difficulties in passing on cost increases

Cost increases and difficulty passing them on mean that a significant proportion of suppliers expect losses in 2022, more than in the previous two years due to COVID-19 and the production shortfall caused by the semiconductor shortage. Nearly one-fifth of suppliers reported losses of more than 5 percent in 2021 and nearly one-third expected losses in 2022. Other suppliers (often in digital technologies and electronics) are showing resilience, with the proportion of suppliers with profitability greater than 5 percent actually doubling between 2020 and 2021.

Nevertheless, more than four in ten automotive suppliers show signs of financial distress, undermining resilience to further external shocks. This figure has worsened, especially in the last three years.

More high-priced cars, fewer cars for Jane and John Doe consumer

But the malaise is spreading further afield. As the profitability of car companies has risen dramatically in recent months due to the high proportion of high-priced vehicles, many corporate headquarters have decided to remove low-priced vehicles from their product lines in the future. The profits made on these vehicles are naturally lower than on premium models.

The car market will change dramatically in the future. This also applies to electromobility and research & development. It is to be feared that it will become a market for the rich and wealthy. For them, rising energy and fuel prices are a nuisance but hardly threatening.

The average consumer, on the other hand, will know how to compensate for the vacuum that will be created in the future – by buying more vehicles from Asia. Chinese manufacturers are well prepared to step into the breach.

The social upheavals caused by changes in production are foreseeable. Fewer vehicles will also require fewer employees.

For European suppliers, on the other hand, the misery will become even worse. They will have to contend with lower volumes and even tighter financial conditions. It is well known that Asia is largely self-sufficient.

It remains to be seen who is the last man standing.

About this column:

In a weekly column written alternately by Eveline van Zeeland, Eugene Franken, Katleen Gabriels, PG Kroeger, Carina Weijma, Bernd Maier-Leppla, Willemijn Brouwer and Colinda de Beer, Innovation Origins tries to figure out what the future will look like. These columnists, sometimes joined by guest bloggers, are all working in their own way to find solutions to the problems of our time. You can read previous episodes here.

Related Posts