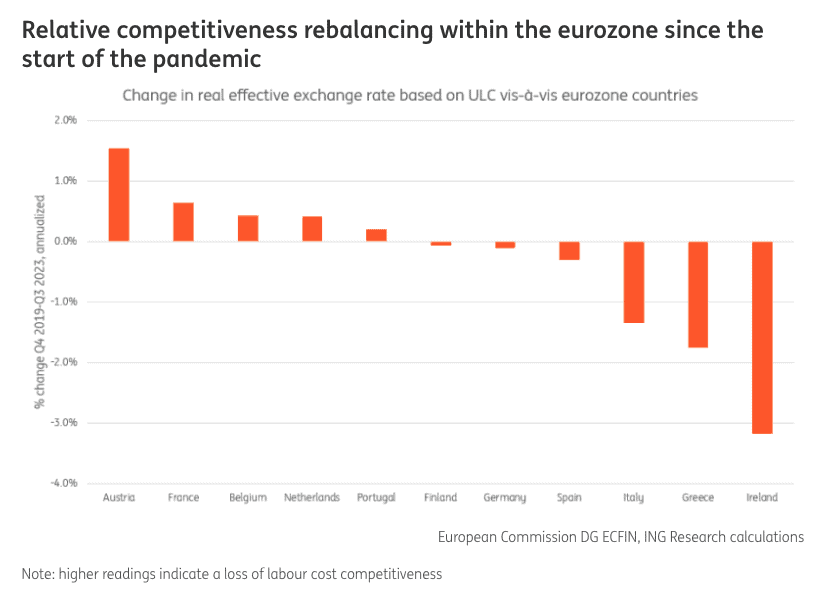

Austria, France, Belgium, and the Netherlands have lost their edge in labor cost effectiveness while their southern counterparts surge ahead. The once-wide gaps in unit labor costs have narrowed significantly post-euro crisis. Germany’s stable performance contrasts with its neighbors’ trends. The pandemic has accelerated this shift, prompting a reassessment of investment patterns and productivity growth. The original eurozone members now grapple with a changing competitive landscape where northern nations must adapt or risk further decline. An ING research report shows huge changes in the balance within the European Union.

Northern Europe was lauded for its economic stability and competitiveness when the European Monetary Union was forged. An intricate web of high productivity, innovation, and efficient labor markets placed these nations at the economic forefront. However, recent data reveals a different narrative. The robustness of northern Europe’s labor competitiveness is faltering in a shifting economic landscape.

Convergence in cost competitiveness

The Eurozone has witnessed a convergence in competitiveness, particularly in relative unit labor costs, a pivotal measure of a country’s workforce cost efficiency. This change has been most pronounced since the start of the Euro crisis, leading to a significant shift in the economic balance within the union.

Austria, France, Belgium, and the Netherlands, once bastions of labor cost competitiveness, have seen their advantages erode. Their average labor costs have risen relative to their outputs, diminishing their competitive edge. In contrast, Germany has maintained a relatively stable position, though it is not without its concerns about future growth.

Italy, Spain, Greece, and Ireland, on the other hand, have improved their standings. These southern European economies have made strides in regaining internal competitiveness, a crucial factor in their economic resurgence. As a result, investments in these regions have markedly increased since the pandemic, signaling renewed confidence in their growth prospects.

Productivity at the core of the issue

The root of this shift in labor cost competitiveness is twofold: investments and productivity. The euro’s first decade saw large capital inflows into the periphery, leading to investments which, in hindsight, were relatively unproductive, ING concludes. This set the stage for the current disparities. Moreover, weak productivity growth in the past decade has exacerbated the issue, particularly in the northern countries.

The pandemic has acted as a catalyst for these underlying trends. Unit labor costs have increased at an accelerated pace in the post-pandemic period, reflecting the urgent need for northern nations to address their waning competitiveness[1]. The investments made since the pandemic have followed a pattern similar to the pre-crisis era, with most periphery markets experiencing massive growth in this area.

Germany’s precarious position

Germany, despite its relative stability, is now referred to as ‘the sick man of Europe’ once again. Concerns about its labor cost competitiveness add to a growing list of worries regarding its growth model. The country that once led Europe’s economy now faces the daunting task of reinvigorating its labor market to fend off the challenge from the rejuvenated South.

As the European Commission DG ECFIN and ING Research highlight, the Netherlands and Austria are the most affected of the original 12 euro countries since the euro’s inception in terms of labor cost competitiveness. This has implications for future investment decisions, as businesses may seek more cost-effective environments, potentially within the southern European markets that have shown significant improvements.

Related Posts