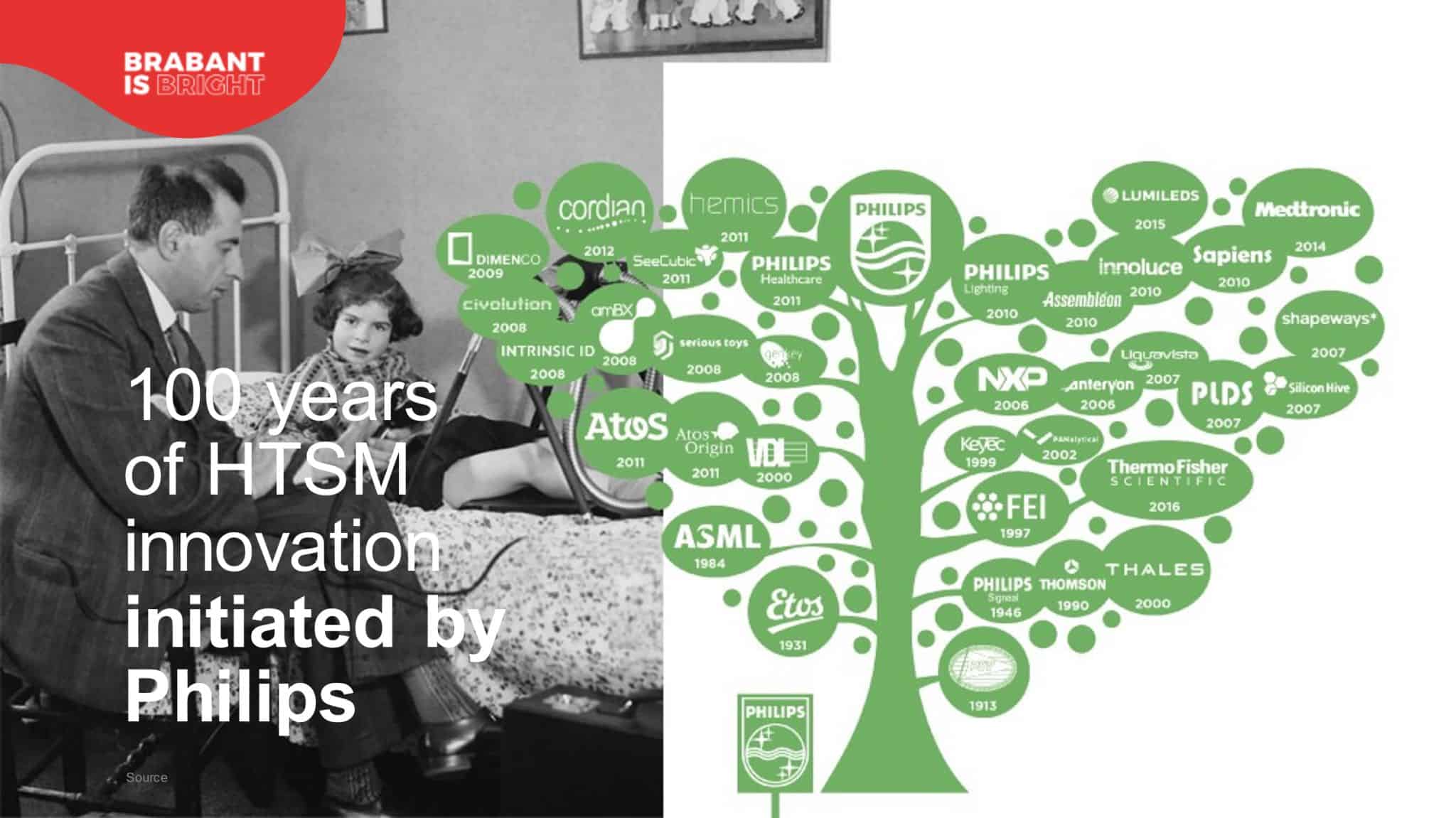

Philips has a history of spinning off divisions like ASML and NXP, now valued at a staggering 450 billion euros. This history overshadows the company’s current focus on medical technology. Despite robust Q4 earnings, Philips’ medical division faces challenges, including a US sales ban on respiratory devices. With spin-offs outperforming their parent company, Philips should consider selling its Medical division entirely. The arguments for selling divisions in the past still hold for Medical. They are not the strongest player in the field, and they struggle, indicating it may not be their core competence.

Selling Medical and focusing on intellectual property (IP) could be a strategic move. Philips could aim to become more like Dolby than GE Health. Instead of abandoning fundamental research, investing more in it could be beneficial. After all, much of Philips’ success stems from fundamental research.

Why you need to know this

Philips once stood as a giant in the Dutch economy, and its legacy, particularly through ASML, remains significant. The path Philips chooses will undoubtedly influence the future of the Dutch economy.

Philips, the Dutch multinational that once dazzled the world with its innovative consumer electronics, has undergone a radical transformation in recent years. The company’s decision to spin off multiple divisions has created industry behemoths like ASML, NXP, and TSMC, whose combined market value now dwarfs their progenitor. But with its medical technology division facing headwinds, the question arises: should Philips continue its legacy of divestment by selling its medical division?

Dissecting Philips’ divestment history

Philips’ divestment strategy is not a recent development. Over the years, the company has shed several divisions, which have continued to prosper independently. For instance, ASML has cornered an 80% market share in the semiconductor industry. The sale of interests in TSMC and ASML alone has led to a situation where these companies are now valued more than Philips. There is a clear pattern: the independence granted to these spun-off entities has allowed them to outperform Philips, suggesting that focus and autonomy are critical ingredients for success.

The challenges facing Philips Medical

Philips’ pivot towards medical technology was a strategic choice to establish the company as a global health technology leader. However, this move has not been without its challenges. The company’s recent history is marred by a significant recall of respiratory devices and a US sales ban following an agreement with the Department of Justice on behalf of the FDA. These setbacks have led to a decline in share price and have cast doubts on the division’s ability to compete effectively in the healthcare market.

Financial performance and market valuation

Financially, Philips has shown resilience with robust free cash flow, but its medical division has yet to deliver the exponential growth witnessed by NXP or ASML. The fourth quarter of 2023 saw an adjusted EBITA margin of 12.5%, yet its valuation lags significantly behind its former components. It prompts the suggestion that Philips, if it were to shed its medical division, could potentially emulate the success of its former parts, leveraging its rich heritage of research and intellectual property (IP) development.

Philips’ future: IP exploitation and fundamental research

If Philips divested its medical division, it could become an intellectual property exploitation company akin to Dolby, focusing on licensing its vast technological innovations. This would be a nod to its legacy, particularly the pioneering work conducted at the legendary NatLab, which has been a cradle for groundbreaking innovations that have reshaped industries. Philips could pivot towards investing more heavily in fundamental research, potentially spawning new technologies and startups, as seen in the Brainport Eindhoven region.

The argument for selling Philips Medical

The argument for selling the medical division builds on the premise that what has worked for the parts may work for the whole. The focus and independence afforded to the spun-off entities have allowed them to outshine Philips. Given the current challenges that Philips Medical is facing, including the loss of sales in the lucrative US market, a divestment could enable the division to flourish under new ownership that might be better suited to navigate the complexities of the healthcare market.

Philips’ heritage and the value of independence

Philips’ heritage is one of innovation and adaptation. The company has repeatedly demonstrated the ability to reinvent itself, and its track record with spin-offs suggests that divestments lead to greater focus and success for the entities involved. Independence is a catalyst for growth, as evidenced by the fact that the spin-offs have not only survived but thrived, outperforming Philips in the market.

Conclusion: A strategic crossroads

Philips faces a decision that could define its future at this strategic crossroads. Selling the medical division could unlock value and allow the company to capitalize on its rich IP portfolio. This would also align with Philips’ history of creating value through focus and independence. While the company has not indicated any plans to sell, the pressure to evolve, given its corporate history and current market challenges, might tip the scales toward another significant divestment.

Related Posts